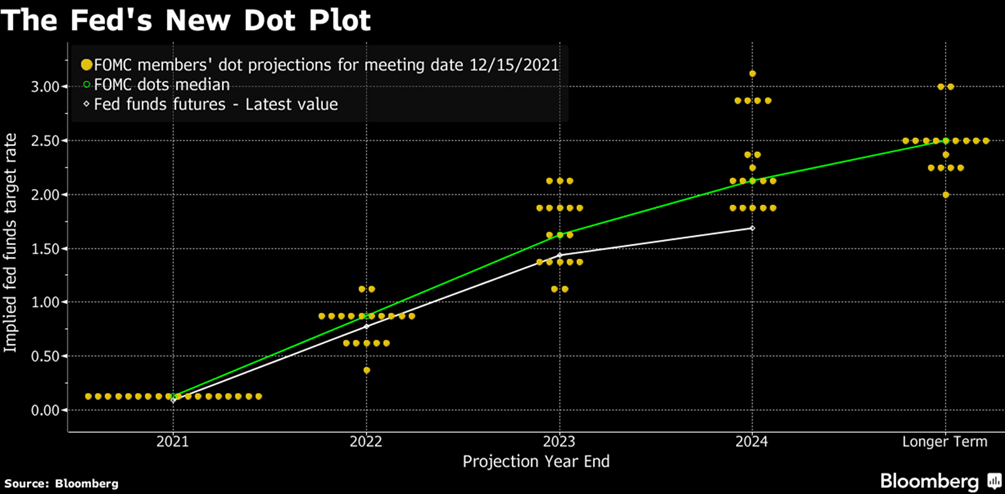

At yesterday’s Federal Reserve meeting, FOMC members announced two important changes to their forward guidance. First, the pace of the tapering of quantitative easing purchases (i.e., the Fed’s purchases of Treasuries and MBS which serve to drive down the cost of issuing additional government debt) will be accelerated to double the speed previously announced at the September Fed meeting. The updated taper schedule now targets to conclude Fed balance sheet expansion in March of 2022. Second, the updated Fed Dot Plot indicates that a majority of FOMC members believe that the Fed Funds rate will be hiked three times in 2022, in 25 basis point increments. This is a significant increase from the September Fed meeting at which median consensus indicated just one rate hike next year, if any at all.

The FOMC has judged that current inflation levels will likely continue to run above its nominal 2% target for some time. In its revised forecast, PCE inflation is expected to be 2.7% in 2022 and remain above 2% in 2023 and 2024, based on expectations that supply chain issues will take a while to resolve. As a reminder, the Fed’s three criteria to consider rate hikes are:

- 2% inflation or higher

- An outlook that inflation will exceed 2% for some time

- Achieving full employment

In his interview after the announcement, Fed Chair Powell acknowledged that although unemployment levels are normalizing, systemic problems remain with labor force participation and businesses continue to struggle to fill open positions. In managing the dual mandate to ensure full employment and stable prices, the Fed has decided that additional progress toward employment is unlikely and will therefore shift focus to controlling inflation.

The Fed’s forward guidance is not a promise but rather an assessment of likely actions made based on current conditions. However, it’s important to note that the Fed is giving this guidance with full knowledge of current concerns, namely the continued toll of COVID-19 variants. This new guidance can be interpreted as a vote of confidence in the future of the US economy in 2022 and beyond. The new tapering schedule would set the Fed to consider their first rate hike in March, but if we see troubling economic data in Q1, they may wait until the May or June meetings. The median consensus points to another three rate hikes in 2023 and a couple more 2024, for a target Fed Funds rate of around 2%.

This updated guidance affirms the signal broadcasted by the announcement of the QE taper in September that the next few years will be a period marked by gradually rising rates. Credit unions largely benefit from a higher rate environment as it allows for more flexibility in potential interest margins. Strategies will need to be adjusted to reposition the balance sheet, and we expect that credit union earnings will improve in the coming years.

This document may contain forward-looking statements based on Accolade Investment Advisory's expectations and projections about the methods by which it expects to invest. Those statements are sometimes indicated by words such as “expects,” “believes,” “will” and similar expressions. In addition, any statements that refer to expectations, projections or characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Such statements are not guarantees of future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict. Therefore, actual returns could differ materially and adversely from those expressed or implied in any forward-looking statements as a result of various factors.