By Phil Lucas

March 9, 2022

Investment strategy can be intimidating when rates are moving, because there’s always a chance that the timing of an individual purchase may look more or less attractive in the following days. Credit Unions are not compensated to speculate on interest rate moves, nor can anyone perfectly time the market. However, in periods of volatility, on days where rates are falling you may consider holding off for a few days to see if yields recover. Likewise, on days where rates are moving upward, you may choose to make a purchase to lock in the upward move. A sound investment strategy should be part of a wholistic balance sheet strategy that ensures stable income regardless of the rate environment.

Last week, Fed Chair Powell testified to the House of Representatives that he supports a single 25 bps rate hike at the March meeting, but other FOMC members have indicated that a 50 basis points increase is still on the table. While it is not possible to divine how markets will react, a 25 basis points increase is the expected outcome of the meeting. This means that after the hike, the yield curve may not look all that different apart from the Fed Funds rate, as rate hike expectations are already priced in. If the Fed decides to hike more aggressively, we’ll likely see short-term rates price up in response, but longer-term rates may sink as a more aggressive Fed hiking schedule may be interpreted as a sign of panicked policymakers. This would further fuel the narrative that the Fed may break something while trying to tighten monetary conditions in an economy that is still normalizing from the events of the last couple of years.

Rate Volatility Presents Opportunities

We continue to see value in considering agency bullets over CDs, particularly at short term tenors of 2 years or less. Even the highest paying issuers of jumbo CDs are paying below Treasury rates as financial institutions look to lock in some term funding before overnight rates increase.

As a reminder, agency bullets are simple bonds issued by the US government or its agencies with no optionality, like CDs. In this space, we’ve consistently found a spread to treasuries and an even higher spread over even the highest-yielding jumbo CDs. If your credit union is using a CD only strategy, you may be leaving significant yield on the table. We’ve been able to consistently find 1 year agency bullets above 1% in recent weeks.

Rate volatility is also directly correlated to the available compensation for call options on bonds. In ordinary conditions, we typically see fixed-rate mortgage-backed bonds such as CMOs (Collateralized Mortgage Obligations, referred to as PACs (Planned Amortization Class) illustrated in the first chart) offer yields superior to callable agencies of similar term. This is due to the higher level of complexity and optionality with an amortizing bond. For example, the bond is prepayable and the cashflows are uncertain month-to-month. However, in recent weeks, the yields between callables and MBS are closing, as more compensation is being offered on the 5-year callables, likely fueled by the market’s uncertainty around where rates will be in the future.

Income vs Flexibility

Most credit unions will find themselves operating an investment strategy under one of two paradigms: the need for current income or the need for more flexibility to reprice for future income. These paradigms reflect the balancing act of managing interest rate risk. Both strategies will likely start to see increases in investment incomes because of how much interest rates have improved. Many credit unions used their interest rate risk budgets through the last two years to support income during a time in which interest margins were compressed, depressed, and overall lousy. For those who need current income, longer-term investments such as callables or CMOs may be appropriate with the acknowledgement that short-term investments may price up and look similar in the future. For the other camp, it may make sense to resume short-term liquidity strategies and rebuild CD ladders while also enjoying higher yields and shedding some upward interest rate sensitivity.

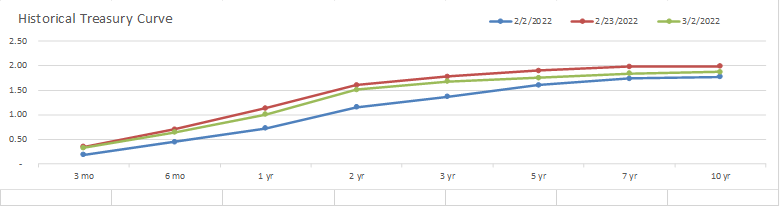

The yield curve continues to flatten. Fed Funds futures indicate a terminal fed funds rate for this hiking cycle of 2- to 2.25%, yet the 10-year has been trading below 2% for most of February 2022. If we see a flat or inverted yield curve, we should interpret that as a warning signal that the market expects a recession soon. In such an environment, the common longer-term investments that we often consider will not offer as much downside protection as we might like. If rates return to zero, callable bonds are called away, and mortgage-backed bonds prepay at higher levels. It may make sense to consider some longer-term bullets as a hedge against a return to zero, which nominally will have lower yields than alternatives, but you may consider that as a premium paid to ensure you can insulate your income streams from another downside shock.

To conclude, we expect interest rates to continue to gradually rise over the next few years. This scenario is priced into the short-end of the yield curve, but the relative flatness of the long-end of the curve indicates that the market worries about growth and inflation prospects. The relative improvement of market yields makes the deployment of excess cash into new investments attractive depending on an individual credit union’s goal. Accolade can help your credit union develop an investment strategy that may optimize your portfolio while mitigating risk in the upcoming rising rate environment.