By Phil Lucas, Senior Balance Sheet Adviser

As members of the FOMC start to signal that the time has come to taper the Fed’s asset purchase program, financial institutions are now preparing for eventual interest rate hikes. In June, the Fed released an updated dot plot showing a majority consensus that expects two 25 basis point hikes to the Fed Funds rate by the end of 2023, for a target range of 50-75 bps for overnight lending. In September, those expectations were bumped up a bit, with half of the FOMC expecting to start hiking rates in 2022. Thus begins the winding down of the Fed’s maximum accommodative policy which signals a transition from the current and indefinite zero-rate environment to a (however slight) rising rate environment.

A zero-rate environment presents significant challenges to balance sheet managers, as potential net interest margins are compressed. Due to those margin pressures, credit unions often look to add longer-term assets or lend down the credit spectrum to support current income. Each of these strategies is accompanied by corresponding risks: the longer-term assets may become unattractive if rates increase in the future, particularly if they are funded by non-maturity deposits, and low-rate environments are typically seen during times of economic stress in which riskier borrowers are less likely to repay loans. The purpose of ALM modeling is to understand the impacts of different interest rate environments on both profitability and capital. While consistent and careful review of these reports is critical to strategy, it is doubly so when interest rate moves are anticipated.

ALM models rely on inputs to project cash flows and market values. Prepayment speed assumptions are applied to relevant accounts to account for the tendency that members prepay loans when interest rates are low but predominantly do not prepay when interest rates are higher or rising. While this behavior is well known, we have found that institutions may be less familiar with how to reconcile expected moves in interest rates with their interest rate risk analysis reporting.

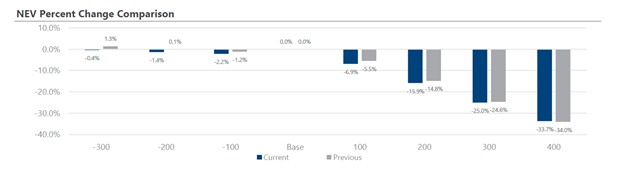

Let’s consider an example. In the below NEV analysis, the credit union is showing an +300 sensitivity of -25% with a base case pointed at Fed Funds being held at the zero range. This means that if interest rates were to move higher by 3% across all points on the yield curve, the Net Economic Value for the credit union would decline by 25%. For many credit unions, this would be considered the threshold between low and moderate risk as defined by board policy. In many ALM meetings, the discussion stops here: the ALM report shows the CU is in policy. However, the +400 scenario could be used to anticipate what the +300 NEV policy limit might look like if Fed Funds was at 1%. Assuming a static balance sheet, the same credit union would have a +300 NEV sensitivity near -34%, which may not be in line with policy or strategy.

You may also notice that the NEV analysis shows a parabolic trend of impairment in higher rate scenarios. Due to the convexity of typical credit union balance sheets, you can see the same relationship between rates and prepayment behavior. Not only do prepayments slow in higher rate scenarios, but the degree by which they slow also increases. To true that up with a practical example, in a zero-rate environment there comes a point for many members where the value of refinancing becomes diminished, but when rates are predominantly higher, a small change in market rates can significantly impact the purchasing power of the borrower.

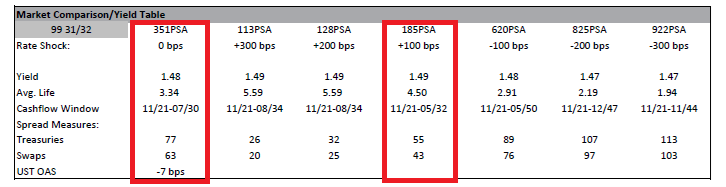

This practice can also be applied to prepurchase analysis for bonds. While we always advocate that a credit union look to purchase investments that perform in line with expectations in all interest rate scenarios, special attention should be placed on the +100 scenario, as it may become our base case before long. In the example below, this bond extends from a 3.3 WAL to a 4.5 WAL in the +100 scenario. However, the price near par ensures that the yield is stable.

This illustrates the importance of proactively considering the changing economic environment when preparing balance sheet strategy. While there is no guarantee that the Federal Reserve will hike interest rates, we as balance sheet managers should set our compasses using the best available market information. A rising rate environment adds additional interest rate risk to credit union balance sheets even if all accounts are held static.