Upbeat economic data raising hopes US economy could skip recession

By Peter Gibson, Chief Investment Officer

Beginning with their first rate hike of this economic cycle in March, 2022, the Federal Reserve has sought to engineer a slowdown in economic growth which would bring inflation back to their long-term goal of 2%. The dramatic speed of rate hikes and monetary policy tightening since then quickly raised recession fears with expectations that 2023 would see the onset of a material economic slowdown. A weak first quarter of economic data supported the thesis that a recession was around the corner, but continued strength in the labor market fueled a rebound in consumer spending which has failed to wilt in the face of higher interest rates.

As we enter the fourth quarter of 2023, those recession expectations are now beginning to recede as American consumers haven’t gotten the memo that they are supposed to be pulling back. From December through June of this year, economists were steadfast in their expectations for an oncoming recession, with 65% of those surveyed consistently expecting a recession within the next twelve months. Since then, recession expectations have been dialed back, with only 55% of economists now forecasting a material slowdown. The primary factor fueling consumers’ ability to continue spending has been the strong labor market, as evidenced by the number of Americans applying for state unemployment insurance.

.png?width=500&height=368)

As the chart above indicates, a rise in initial claims for jobless benefits followed a large round of announced layoffs earlier this year. But since June, the number of individuals filing claims for those benefits has continued to drop as employer layoffs abated and hiring has rebounded, with September’s payroll growth of 336,000 outpacing all economist expectations.

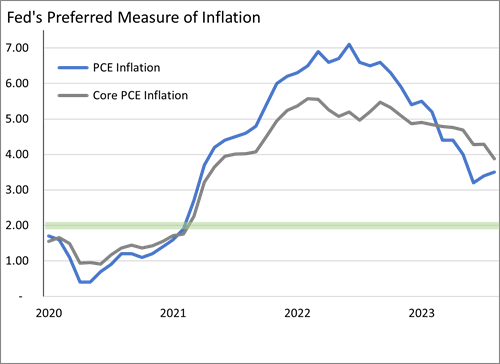

However, this strong rebound could prove to be its own undoing as the Federal Reserve is committed to pushing inflation lower. Despite the improvement in inflation measures over the past year, annual inflation is still running above target at approximately 4% using the Federal Reserve’s preferred price measure. Of note, the headline PCE inflation measure (in blue below) has actually risen the last two months, an unwelcome development for policymakers.

The combination of a nascent economic recovery amid a continued tight monetary policy environment has many economic forecasters wondering if the US economy can indeed thread the needle and return to its long-term growth path without entering a recession. This has proved an elusive goal for Fed policy makers in previous monetary policy tightening cycles. The recent economic data has resulted in the base case expectation that interest rates will need to stay at these relatively high levels longer than previously forecast in order to bring down inflation, with the outside chance that additional rate hikes may be needed.

This means that credit unions should be prepared for the current rate environment to persist through the remainder of the year and through much of 2024. While Fed funds futures are currently indicating a potential rate cut in mid-2024, inflation statistics do not support such a forecast and will need to materially improve in order to bring possible rate cuts on to the Fed’s agenda. The high rate environment will likely keep liquidity pressures high, as depositors with large balances look for higher yields available in CDs or money market funds.

We at Accolade are committed to helping your credit union succeed, if you would like to learn more about this topic, please reach out to your Accolade investment adviser representative.