What are Mortgage-Backed Securities?

The US mortgage marketplace is dominated by loans guaranteed by three entities: Ginnie Mae, Fannie Mae and Freddie Mac. These entities enable mortgage securitization by removing credit risk to investors via their guarantee. Ginnie Mae bonds carry the full faith and credit of the United States. Fannie and Freddie are government sponsored enterprises which do not carry an explicit guarantee, but instead, an implicit government guarantee. Since 2008, both GSE’s have been conserved by the US Treasury with all profits directed to the government. Due to the difference in guarantee, Ginnie Mae bonds trade slightly more expensively, all else equal.

Collectively we refer to the mortgage-backed securities guaranteed by these entities as Agency MBS, and the collateralized mortgage obligations constructed off these securities are referred to as Agency CMOs. These entities guarantee a large variety of loans, but the primary residential collateral types are 30-year fixed mortgages, 15-year fixed mortgages, and ARMs (e.g., 5/1 or 7/1 ARMs). 30-year fixed mortgages make up about 90% of current origination. Commercial loans are also guaranteed, but the security level analysis is significantly different than residential collateral.

For Agency MBS, individual mortgages are combined into pools with loans of similar characteristics, often along maturity, coupon, age, and loan size groupings. Some factors are often not standardized across pools such as the number of loans and geographic concentrations. When analyzing Agency MBS pools, it is important to consider how mortgage prepayment speeds change the key characteristics of the bond such as average life profile, yield performance, and overall interest rate risk. Any unique factors that may cause the pool to prepay faster or slower than consensus speeds should be evaluated as well as relative value versus other fixed income asset classes.

Advantages and Disadvantages

The advantages of purchasing Agency MBS are often higher yields than investments with similar interest rate risk. The amortizing cashflows provide liquidity, augment a laddered portfolio strategy, and reduce reinvestment risk.

Disadvantages included premium risk, cashflow length (as long as the underlying mortgages), and prepayment sensitivities to interest rate changes.

Why create CMOs out of MBS pools?

Investors are limited by available Agency MBS pools, giving them very little choice of average life profile. Additionally, mortgage coupons are typically higher than current market rates which results in a premium price for the bond after wrapping the bond with a guarantee. Certain CMO structures can offer investors a bond priced closer to par with stable yield performance. Lastly, MBS pools are fully exposed to changes in prepays and may offer an unpredictable cashflow structure.

Cashflow Structure

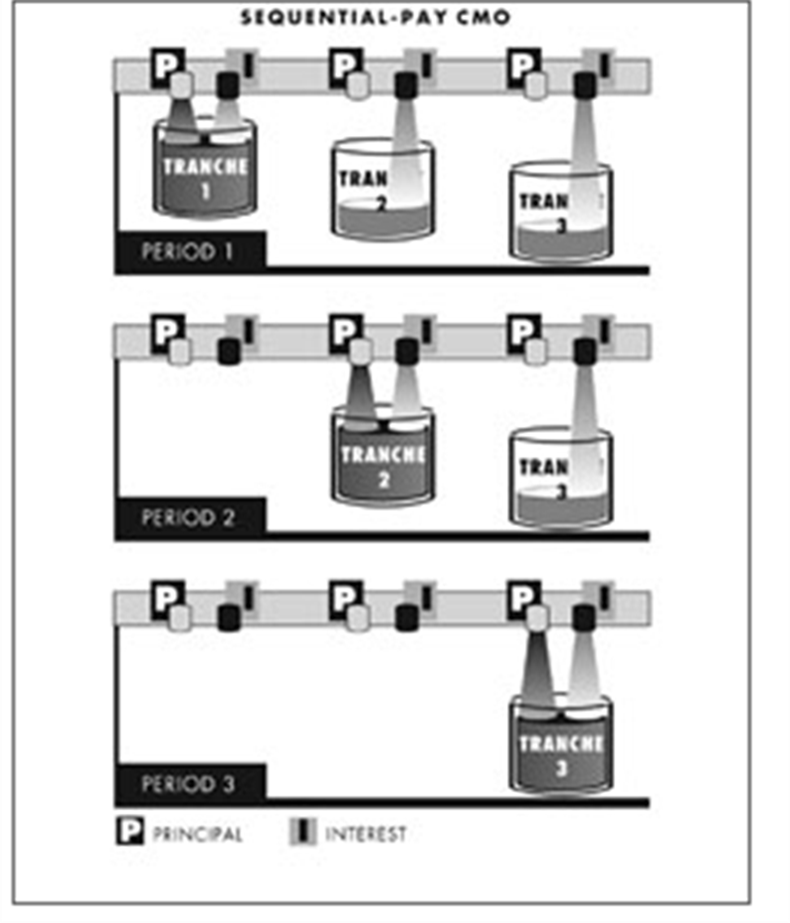

CMOs frequently change the cashflow or coupon structure of a pool (or many pools) of mortgage-backed securities in order to better tailor an investment to an investor’s needs. For example, a sequential pay CMO redirects principal payments from underlying mortgage pools to pay down CMO tranches in sequence, one after the other. This offers a better tailored investment for investors who desire short-term cash flow windows (e.g., financial institutions) and to those who desire the opposite (e.g., insurance companies).

Figure 1. Sequential Pay CMO Illustration

Another common structure is a Planned Amortization Class (PAC) CMO which is constructed to deliver consistent cashflows every month within a predetermined prepayment speed band. With this structure, monthly principal payments are directed to the first PAC tranche up to its target size. As long as mortgages amortize as planned, monthly principal cashflows will be the same until the bond is paid off.

Interest Reallocation

We can also achieve interest reallocation via CMOs by constructing floating-rate investments off of fixed-rate MBS pools. A floating-rate tranche is created and offset by a speculative inverse floating-rate tranche which is often attractive to interest rate speculators like hedge funds. Floaters offer lower interest rate risk and allow investors to benefit from a rising rate environment. Frequently, floating-rate CMOs also have sequential or PAC structures as well.

Advantages and Disadvantages

Agency CMOs offer the ability to create an investment profile which better fits investors needs and can often offer higher yielding versions of MBS cashflows with similar characteristics.

The disadvantages include more variability in structures, requiring deeper analysis and understanding, and lower liquidity than MBS pools. When analyzing CMOs, brokers sometimes manipulate yield tables to optimize the appearance of the bond and it is critical for investors to have the tools and education to properly analyze these securities.

Agency MBS and CMOs contain additional risks beyond GSE debentures and callables but when priced appropriately, they can deliver excess risk-adjusted returns. To learn more about fixed-income investments strategies for credit union investors, please reach out to Accolade’s investment advisory team.

Author: JD Pisula