By: Peter Gibson, Chief Investment Officer

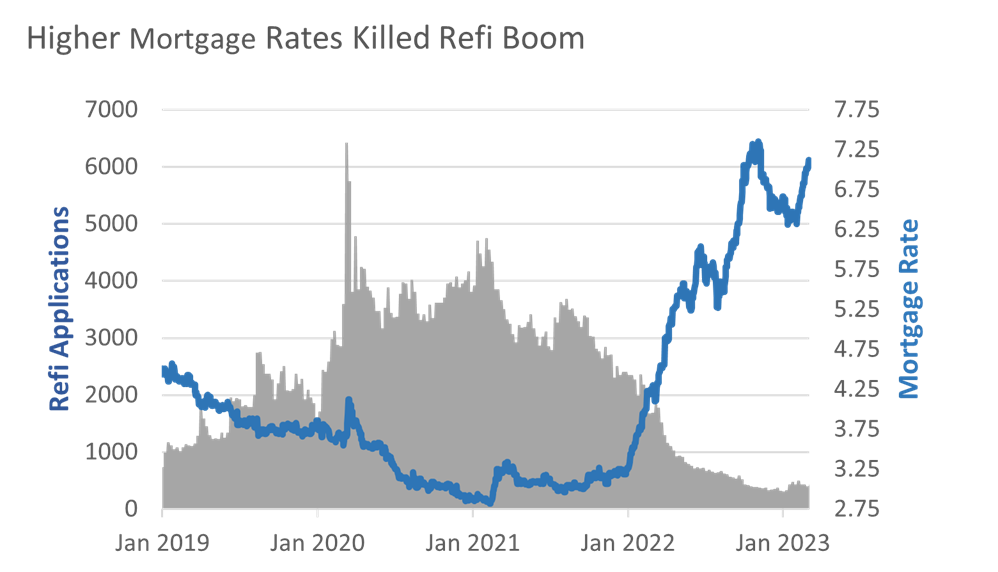

A combination of structural and seasonal factors are currently depressing prepayment speeds, resulting in the extension of mortgage-backed securities and CMOs. The combination of persistently high inflation and the Federal Reserve’s historically quick rate tightening has lifted longer-term yields and slowed mortgage prepayments, lengthening assets at many credit unions. With 30-year mortgage rates currently near their highest levels in the past twenty years (currently revisiting the range of 7.00%+ levels, initially breached last fall), virtually all mortgages on credit union’s books are exhibiting very low prepayment speeds.

.png?width=600&height=363)

The chart above indicates that prepayment speeds have converged for 30-year mortgages across a wide cross-section of rates, leading to similar average life profiles for mortgages with coupons ranging from 3.25% to 5.25% and even higher (net coupons on MBS pools are generally 50-75 bps below the actual mortgage rate paid by the homeowner). For example, a prepayment speed of 5 CPR means that on an annualized basis, 5% of the loan balance will be prepaid over the coming twelve months. This is an exceptionally low level of prepayments which reflects the lack of any refinancing incentive as well as a tight housing market resulting from the combination of strong price appreciation and the increase in mortgage rates. This has left many homeowners reticent or unable to list existing homes for sale because it is increasingly difficult to acquire a new house without absorbing a very significant increase in monthly payments.

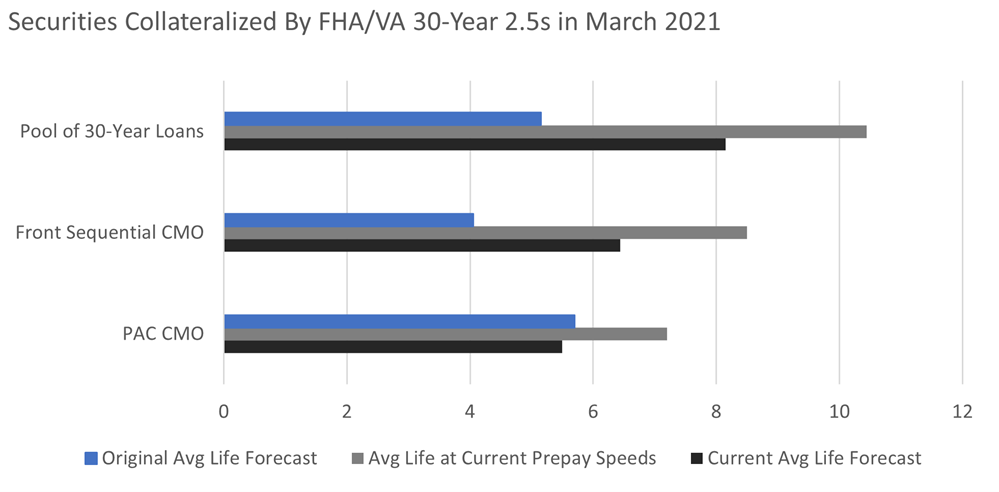

Mortgages and mortgage-backed securities (MBS) make up a meaningful portion of many credit unions’ balance sheets. Now that rates have climbed even more than the +300 bps “worst case” rate scenario that typically accompanies most investment decisions, the timing seems appropriate to revisit the potential value added by purchasing structured mortgage-backed securities. Here, we do so by examining MBS and structured mortgage-backed securities (CMOs) originated at the trough of rates in March 2021. At that point in time, the average 30-year mortgage was being originated at a rate just above 3.0%. In that month, Ginnie Mae issued a series of CMOs (GNR 2021-44) which proves instructive when examining the impact of the subsequent increases in interest rates have had on both those bonds as well as the underlying 30-year mortgage collateral.

Mortgages and mortgage-backed securities (MBS) make up a meaningful portion of many credit unions’ balance sheets. Now that rates have climbed even more than the +300 bps “worst case” rate scenario that typically accompanies most investment decisions, the timing seems appropriate to revisit the potential value added by purchasing structured mortgage-backed securities. Here, we do so by examining MBS and structured mortgage-backed securities (CMOs) originated at the trough of rates in March 2021. At that point in time, the average 30-year mortgage was being originated at a rate just above 3.0%. In that month, Ginnie Mae issued a series of CMOs (GNR 2021-44) which proves instructive when examining the impact of the subsequent increases in interest rates have had on both those bonds as well as the underlying 30-year mortgage collateral.

At that time, the MBS pool and two CMO’s constructed from the collateral were originated with roughly similar base case average lives with just the sequential CMO expected to prepay more quickly with an average life near four years. As would be expected from the subsequent increase in interest rates, the average life at current prepay speeds has lengthened significantly on the pool as there are no structural enhancements to protect the bondholder from the dramatic decline in prepayment speeds. The sequential CMO has not fared significantly better despite the protection offered by a rear sequential bond, with a current average life nearly double the original projections. While the structural advantages of the PAC structure did not fully protect the bond from extension risk, the bond did offer material extension protection when compared to the collateral or the less-structured sequential CMO. While the specific construction of individual sequential or PAC CMOs can vary greatly, the example above demonstrates that, in this case, the PAC structure was able to offer greater protection in an adverse rate environment.

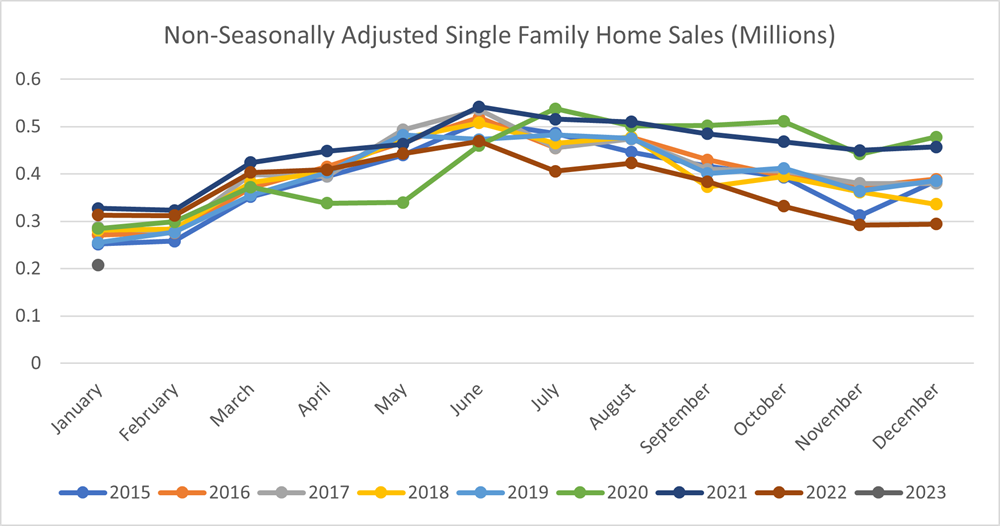

Despite the longer average lives implied by the very low level of current prepayment speeds, there is some reason for hope as the current rate and home sales environment is not expected to persist indefinitely. As the black bars above indicate, current estimates of remaining average lives imply a meaningful pickup in prepayment speeds as rates and home prices normalize, while homes sales will likely contribute to higher levels of housing turnover later in the year. While mortgages originated over the past few years are certainly not forecast to prepay at the high speeds seen during the pandemic, the very slow current speeds look to be the nadir of MBS extension as they are partially depressed by seasonal factors that should abate in the coming months.

The early part of the year is traditionally the slowest period for housing sales and 2023 has been no exception. With only 208,000 units sold (on a non-seasonally adjusted basis), it is reasonable to forecast higher home sales throughout the spring selling season, which will feed directly into prepayment speeds as existing homes are sold. While this will not be a panacea for the high average lives currently observed in credit union MBS portfolios, it should help at the margin by lowering portfolio average lives while providing some additional liquidity.

After experiencing the largest yield curve shock in decades, mortgages are approaching maximum extension with prepayment speeds near floors. By properly evaluating extension and contraction risks upfront, credit unions can proactively mitigate these risks while adding reliable amortizing cashflows to their balance sheet. We at Accolade are committed to helping your credit union succeed, if you would like to learn more about this topic, please reach out to your Accolade investment adviser representative.